The video gaming sector is a $195.6 billion dollar industry with a predicted CAGR of 14% through 2030 – and during the last recession, back in 2008, it continued to see strong sales growth.

Games have a number of attributes that contribute to their success in down-bound markets. To start with, customers will continue to buy gaming products, and once purchased, games can continue entertaining over an extended period of time. Many gaming companies also offer free-to-play games, online or for download, that function as loss-leaders, and the gaming companies can still profit from in-game purchases and paid online ads.

The upshot of it all is that the gaming sector may offer investors a sound defensive position in a recessionary environment. We can follow that logic, taking a cue from Southeast Asia’s largest bank, Singapore’s DBS, which has been tagging the giant gaming stocks as Buys, with upside potential on the order of 20% or better. DBS is not alone in its upbeat assessment; according to the មូលដ្ឋានទិន្នន័យទិព្វរ៉ានស៍, both are rated as Strong Buys by the analyst consensus, too. Here are the details, along with commentary from DBS.

Electronic Arts, Inc. (EA)

We’ll start with Electronic Arts, a $34 billion giant of the gaming sector. The company, based in Silicon Valley, boasts a strong portfolio of games, including such titles as អ្នករស់រានមានជីវិត Jedi, FIFA បាន 23, Madden 23និង មេដាយកិត្តិយសខាងលើនិងលើសពីនេះ។. Electronic Arts benefits from owning copyrights on numerous popular game franchises, and from its lucrative agreements with professional sports leagues.

During 2022, EA shares slipped, like much of the tech sector, but by only 7%, meaning EA outperformed the NASDAQ index by a factor of 5. This relative outperformance came as EA also showed year-over-year gains on several key metrics. In the most recent financial release, for Q2 of fiscal year 2023 (the quarter ending on September 30), EA showed a top line revenue of $1.9 billion, up 5% from the $1.8 billion reported in fiscal 2Q22. This revenue was supported by generally strong business, including net bookings for the trailing 12 months of $7.38 billion, a total that was up 4% y/y.

At the bottom line, EA’s net income came in at $299 million, compared to $294 million in the prior-year quarter, with EPS being reported at $1.07 for a 5% y/y gain.

Covering this stock for DBS, analyst Tsz Wang Tam sees the company in a solid position to continue growing, even as video game demand slows post-COVID, with a particular advantage coming from the sports game franchises. He writes, “The pandemic has accelerated the adoption of digital games, live services, and new platforms. Electronic Arts (EA)’s games and products enable the company to catch the expanding demand in various countries and regions, leading to above-peer average EBITDA growth of 26%…. EA has a large sports franchise and 300+ exclusive licenses to publish football simulation video games. EA’s largest game FIFA has dominated the sports game market. Besides, EA has a robust pipeline with sports games scheduled for release, which will drive growth over the coming years.”

Following from this stance, Tam gives the stock a Buy rating, with a $165 price target to suggest a one-year upside potential of 32%.

The Strong Buy consensus rating on EA is based on 10 recent Wall Street analyst reviews, with an 8 to 2 breakdown favoring Buy over Hold. The current trading price is $125.01, and the average price target of $149.60 implies a 20% upside for the coming year. (See Electronic Arts’ stock forecast at TipRanks.)

Activision Blizzard (ATVI)

Next up is an old name in the gaming business, Activision Blizzard. This is one of the world’s largest gaming companies, with a $60 billion market cap, and under the Activision name it dates back to the earliest days of home computer video gaming – some of Activision’s first titles were released for cartridge-loaded game consoles in the early ‘80s. Today, Activision Blizzard is the owner of such major online game titles as ពិភពលោកនៃ Warcraft, ការហៅរបស់កាតព្វកិច្ចនិង ល្បែងខេនឌីក្រាស់. The company operates through esports, consumer products, and media divisions.

The biggest news over the past year for Activision Blizzard was the announcement, in January of 2022, that tech giant Microsoft was targeting the gaming firm for acquisition, with Microsoft proposing a $68.7 billion all-cash transaction. In the most recent update, on December 8, Activision Blizzard’s CEO announced that the Federal Trade Commission was filing suit to block the merger. Both companies are challenging the regulatory authority’s action.

Even after news of the regulatory challenge to the proposed merger, ATVI shares remain strong. The stock gained 14% in 2022, and in the last reported quarter, 3Q22, the company beat expectations on both revenue and earnings. While the top and bottom lines both fell year-over-year, the $1.78 billion in revenue was 4.7% above the forecast, and the 55-cent GAAP EPS did even better, beating expectations by 31%.

Checking in again with Tsz Wang Tam, for the DBS view, we find that the analyst has outlined a solidly bullish position on Activision Blizzard shares, saying of the company’s prospects, “Activision Blizzard is well positioned to capitalize on its game properties via live service offerings, which allow players to access and invest in new content and increase engagement. Currently, live service (or in-game purchase) revenue makes up 38% of total revenue, mainly contributed by Candy Crush. The continuous focus on in-game content and live service development will generate higher revenue with a higher margin…. We expect mobile games to become a significant revenue growth engine in the coming years, driven by the robust mobile game pipeline and increasing addressable audiences.”

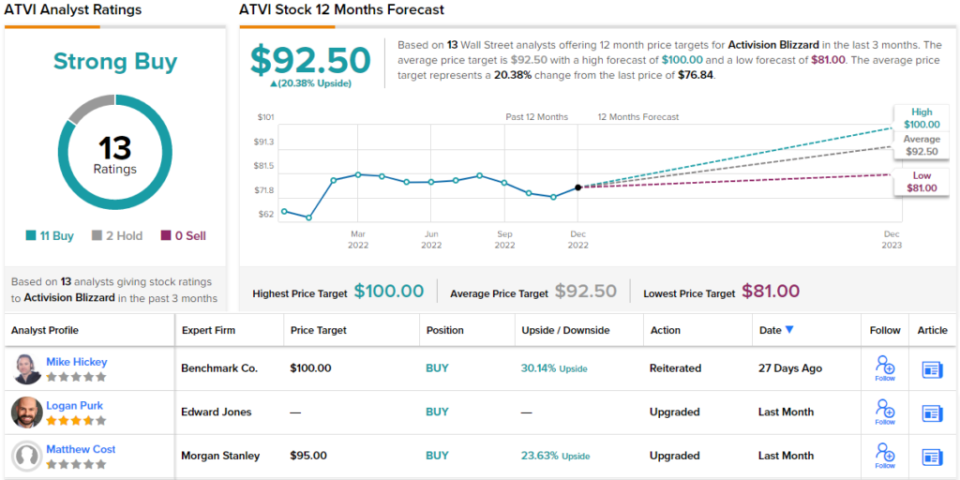

These comments come with a Buy rating, and Tam’s $92 price target implies a 12-month upside potential for the stock of 20%.

Activision Blizzard finds support for its Strong Buy consensus rating from 13 recent analyst reviews, including 11 to Buy and just 2 to Hold. The average price target of $92.50 is almost the same as Tam’s objective. (See Activision Blizzard’s stock forecast at TipRanks.)

ដើម្បីស្វែងរកគំនិតល្អ ៗ សម្រាប់ការជួញដូរភាគហ៊ុនក្នុងការវាយតំលៃដ៏គួរឱ្យចាប់អារម្មណ៍សូមចូលទៅកាន់គេហទំព័រទិព្វរ៉ាថេក ភាគហ៊ុនល្អបំផុតដើម្បីទិញដែលជាឧបករណ៍ដែលទើបបង្កើតថ្មីដែលបង្រួបបង្រួមរាល់ការយល់ដឹងអំពីសមធម៌របស់ទិព្វរ៉ានស៍។

ការបដិសេធៈមតិយោបល់ដែលបានលើកឡើងនៅក្នុងអត្ថបទនេះគឺគ្រាន់តែជាគំនិតរបស់អ្នកវិភាគដែលមានលក្ខណៈពិសេសប៉ុណ្ណោះ។ ខ្លឹមសារមានគោលបំណងប្រើប្រាស់ក្នុងគោលបំណងផ្តល់ព័ត៌មានតែប៉ុណ្ណោះ។ វាមានសារៈសំខាន់ខ្លាំងណាស់ក្នុងការធ្វើការវិភាគដោយខ្លួនឯងមុនពេលធ្វើការវិនិយោគ។

Source: https://finance.yahoo.com/news/2-gaming-giants-double-digit-090446813.html